A lot of advice out there sounds good on paper but fails to work in reality.

Follow your passion!

Sure, but does your love of fantasy football pay the bills?

You can do anything you set your mind to!

Tell that to my 5th-grade NBA dreams.

The same is true of some financial advice. It sounds good as an inspirational quote but ends up being more or less impossible to pull off in real world for most people.

For example — ignore the noise. Excellent advice. They hand this quote out to financial advisors the day they earn their CFP.

And it’s impossible to follow in the information age.

Everyone now has a supercomputer in their pocket that’s a constant barage of alerts, news, messages and social media posts about what’s going on in the world. The news is everywhere. You can check stock prices, track your performance and place trades immediately and without thought.

Ignoring the noise is not a viable strategy today.

What you need is a good process to filter out the noise. You have to figure out the right voices to follow and understand the difference between actionable advice and financial entertainment.

You can’t ignore the noise anymore but you can find ways to avoid overreacting to it.

Here are some more pieces of financial advice that sound useful but aren’t realistic:

Don’t look at your statements. Yeah right! Everyone looks. Maybe just don’t look during bear markets.

Just wait for the fat pitch. Markets are moving faster than ever. You don’t have as much time to wait around for the fat pitch as you used to. Plus, valuations are higher now than they were in the past.

The long-term average CAPE ratio going back to 1871 is 17.6x. Do you know how often the market has been trading below that uber-long-term average for in the past 30 years?

Just 10 months out of 360 in total, or less than 3% of the time. And all 10 of those months were in 2008 and 2009 during the Great Financial Crisis.

Waiting for the fat pitch sounds like an awesome idea until you realize the market doesn’t wait around for you to be comfortable enough to invest.

You’re better off investing on a regular basis and avoiding the brain damage that comes from trying to time the market.

You need 12 months of living expenses in your emergency fund. This is something only rich personal finance experts say.

How many people have the ability to put their life on hold to the extent that they can actually set aside that much money? It’s a worthy goal but impossible for most households.

You definitely need an emergency fund but I don’t think you should live like a hermit or forgo other goals to make it a reality.

I like the idea of having other financial backstops — a home equity line of credit, a brokerage account, Roth contributions, etc. — as you slowly but surely increase your emergency fund over time.

Pay off your mortgage early. There is a case to be made for paying down your mortgage early if you just borrowed at 7%. But I think it’s crazy for anyone who was able to borrow at 5% or less before rates shot up.

I wish I would have taken out more debt in the early 2020s. My 3% mortgage will likely go down as one of the best financial assets I ever hold and it’s actually a liability!

A fixed rate mortgage is a wonderful financial tool if used the right way. After accounting for inflation and tax write-offs, it’s a pretty good deal even if you’re forced to borrow at higher lending rates these days. Some day you’ll be able to refinance.

I know some people are allergic to debt. If you have a 3% or 4% mortgage I can’t think of a single good reason to pay it off.

Put 20% down before buying a house. With housing prices so high a 20% down payment simply isn’t feasible for most first-time homebuyers.

If we’re forcing people to put 20% down AND set aside 12 months of living expenses AND max out your 401k that’s like 5% of the population, maybe.

It’s sound advice but not possible for most households.

If you want to buy a house with 5-10% down and you can afford the monthly payment there is nothing wrong with that.

The down payment on our first home was 5%. It worked out and we didn’t have to wait forever to buy a house while we saved for a bigger down payment.

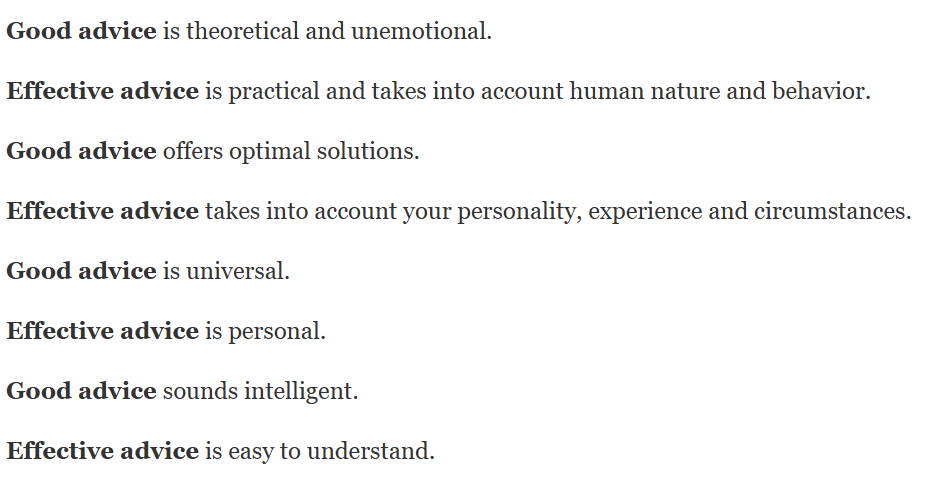

There’s a big difference between good advice and effective advice.

It would be wonderful if everyone was as unemotional as Mr. Spock and always made the perfectly rational decision. Perfect is often the enemy of good when it comes to your finances.

Good advice is theoretical and unemotional.

Effective advice is practical and takes into account human nature and behavior.

Good advice offers optimal solutions.

Effective advice takes into account your personality, experience and circumstances.

Good advice is universal.

Effective advice is personal.

Good advice sounds intelligent.

Effective advice is easy to understand.

Michael and I talked about financial advice, fat pitches, the housing market and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Also this week I had Nick Maggiulli on The Unlock to discuss giving strategies, spending, inheritance and tax planning in retirement:

If you’re an advisor, sign up for The Unlock newsletter for all things wealth management.

Further Reading:

The Worst Kind of Financial Advice

Now here’s what I’ve been reading lately:

Books: